Non-Linear Alpha Signal Ranking (NLASR)

Apr 22, 2026 - Tribhuven Bisen

A Comprehensive Framework for Alpha Aggregation

Non-Linear Alpha Signal Ranking (NLASR)

A Comprehensive Framework for Alpha Aggregation

Quant Insider April 21, 2026

1 Introduction

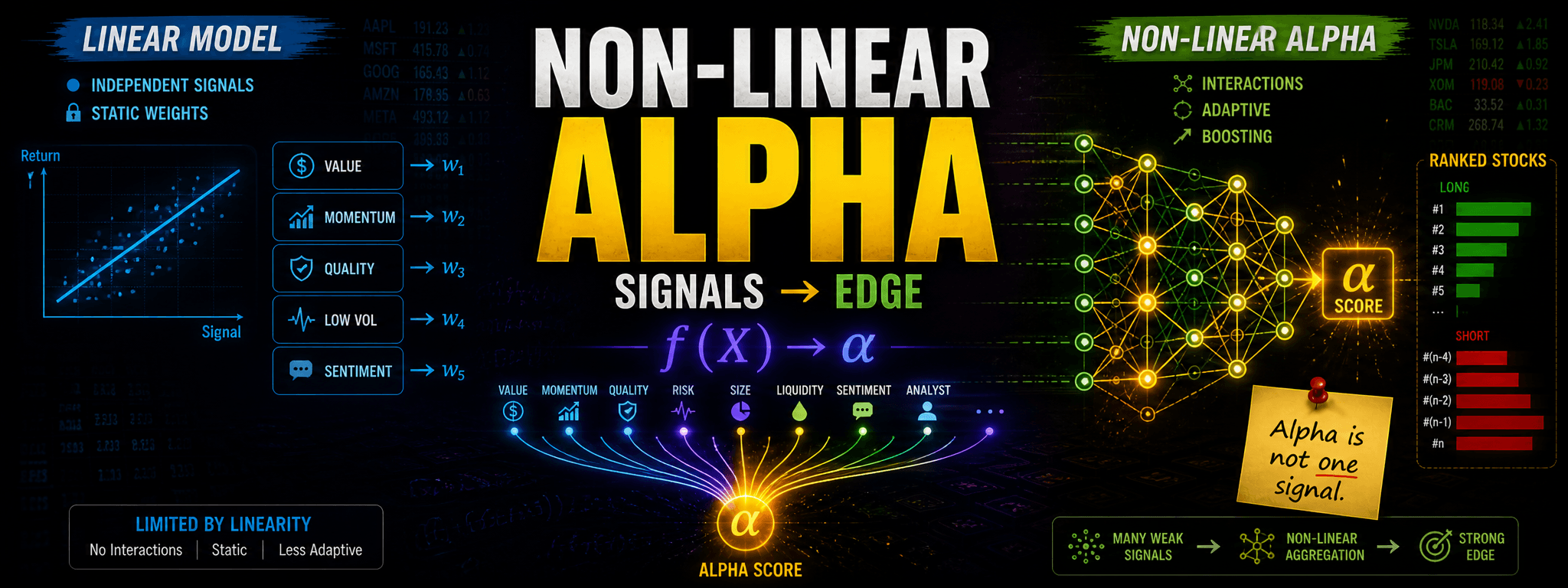

Modern quantitative equity strategies rely on extracting predictive signals from a large and diverse set of features. Individually, these signals tend to have low signal-to-noise ratios, but collectively they can produce meaningful alpha.

Non-Linear Alpha Signal Ranking (NLASR) is a machine learning-based framework designed to:

- Aggregate a large number of weak signals into a unified alpha score

- Capture non-linear interactions across factors

- Adapt dynamically to changing market regimes

- Improve robustness and diversification in stock selection

The key philosophy is that alpha is not concentrated in a single signal, but distributed across many weak, unstable predictors.

2 Core Idea: From Linear to Non-Linear Alpha Aggregation

Traditional factor models assume a linear structure:

This approach implicitly assumes:

- Factor independence

- Constant factor premia

- Linear contribution of each signal

However, empirical evidence suggests:

- Factor premia are time-varying

- Factor interactions are non-linear

- Signal effectiveness is regime-dependent

Hence, we require a mapping:

where is non-linear and adaptive.

3 Feature Library: The Alpha Factory

3.1 Philosophy

Instead of selecting a small number of "best" signals, NLASR adopts a feature abundance approach, often referred to as a "kitchen sink" methodology.

3.2 Feature Categories

-

Valuation Signals:

- Book-to-price, earnings yield

- Capture long-term mispricing

-

Momentum Signals:

- Price momentum (12-1, residual)

- Reflect behavioral biases and underreaction

-

Quality Signals:

- Profitability, margins, earnings stability

- Capture fundamental strength

-

Risk Signals:

- Volatility, beta, drawdown metrics

- Capture risk premia

-

Balance Sheet Signals:

- Leverage, liquidity, capital structure

-

Alternative Data Signals:

- Sentiment (news, social media)

- Analyst revisions

- Corporate activity

3.3 Insight

Each signal:

- Has low standalone predictive power

- Works only in certain regimes

- Contains noisy but valuable information

Key Insight: The goal is not to find perfect signals, but to combine imperfect signals intelligently.

4 Data Preprocessing and Normalization

Features are standardized cross-sectionally:

4.1 Why this matters

- Removes scale differences

- Ensures comparability across signals

- Prevents dominance of high-variance features

5 Boosting Framework

5.1 Motivation

Boosting converts weak learners into a strong learner by sequentially focusing on difficult observations.

5.2 Model Structure

5.3 Interpretation in Alpha Context

- : weak signal (factor or transformation)

- : importance of signal in current environment

5.4 Key Insight

Boosting naturally performs:

- Feature selection

- Non-linear interaction modeling

- Dynamic weighting of signals

6 Non-Linearity and Interaction Effects

6.1 Why Non-Linearity Matters

Financial signals rarely operate independently.

Example:

- Momentum works only when volatility is low

- Value works after market stress

This implies:

6.2 How NLASR Captures This

- Sequential reweighting

- Implicit feature interactions

- Conditional decision boundaries

7 Factor Momentum: A Critical Layer

7.1 Concept

Factors themselves exhibit persistence:

7.2 Practical Insight

- Momentum factor dominates in trending markets

- Value factor dominates in recovery phases

7.3 Implication

The model must:

- Increase weight on winning factors

- Reduce weight on losing factors

Boosting achieves this naturally.

8 Training Methodology

8.1 Multi-Horizon Training

Models are trained on multiple windows:

- Short-term: captures recent trends

- Medium-term: captures cyclical behavior

- Long-term: captures structural relationships

8.2 Insight

This creates:

- Model diversification

- Regime robustness

8.3 Avoiding Overfitting

- Time-series cross-validation

- Out-of-sample validation

- Regularization in boosting

9 Alpha Score Construction

Final alpha score:

9.1 Interpretation

- High score → strong expected outperformance

- Low score → expected underperformance

9.2 Ranking

10 Portfolio Construction

10.1 Strategy Design

- Long top decile

- Short bottom decile

10.2 Enhancements

- Sector neutrality

- Beta neutrality

- Risk budgeting

10.3 Insight

The model does not predict absolute returns, but relative ranking.

11 Why NLASR Works

- Aggregates many weak signals → reduces noise

- Captures non-linear relationships

- Adapts to market regimes

- Exploits factor momentum

- Diversifies across signals

12 Limitations and Risks

- Data quality dependence

- Model complexity

- Reduced interpretability

- Risk of regime breakdown

13 Conclusion

NLASR represents a modern approach to alpha generation, shifting from static factor models to adaptive, data-driven frameworks. By combining a large feature library with a boosting-based architecture, it provides a scalable and robust solution for stock selection in complex market environments.