Practical Guide to Gamma Greeks

Apr 22, 2026 - Tribhuven Bisen

The blog explains how to compute and use Gamma and higher-order Greeks to manage hedging, volatility sensitivity, and risk dynamically in options trading.

Abstract

This article explains how to compute and use Gamma and related second- and third-order Greeks in real-world option trading and risk management. Included are:

- How to calculate standard Gamma () and interpret it in practice

- Approximations for fast evaluation (Saddle Gamma)

- Normalizing Gamma (GammaP) for position sizing

- Using Gamma symmetry for skew analysis

- Evaluating sensitivity of Gamma to volatility (VommaGamma)

- Using Speed () for dynamic hedging

- Using Color () to understand time decay of risk

Throughout, we show numerical examples and discuss how traders and risk managers incorporate these metrics into daily workflows.

1 Introduction

Gamma is a critical measure for understanding how an option’s Delta changes with small moves in the underlying. In practice, high Gamma positions require frequent rebalancing to remain hedged. This guide provides step-by-step formulas, numerical examples, and notes on how to integrate Gamma-related Greeks into trading systems and risk reports.

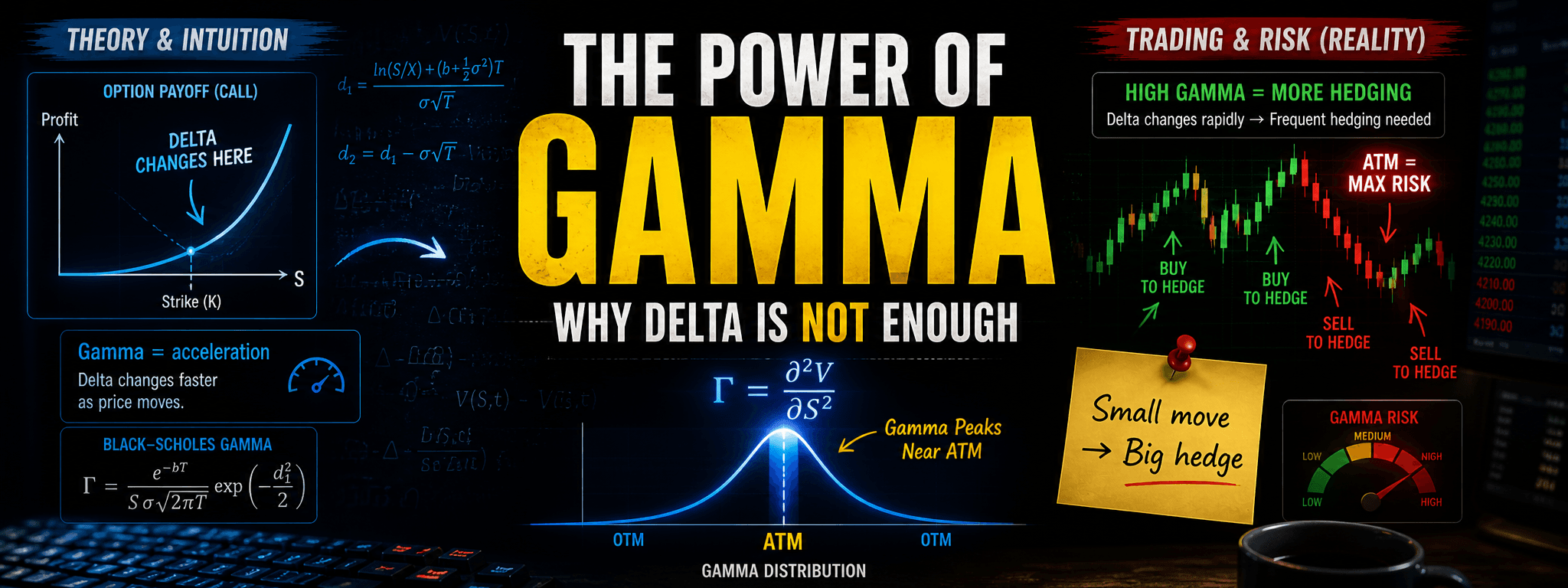

2 Standard Gamma: Calculation and Example

2.1 Formula

Under Black-Scholes, the Gamma for a European call or put is:

where

and

- S: current spot price of the underlying

- X: option strike

- T: time to maturity (in years)

- b: cost-of-carry (for stocks, typically r − q, where q is dividend yield)

- σ: implied volatility (annualized)

2.2 Numerical Example

Suppose:

- Underlying S = 100

- Strike X = 100

- Time to maturity T = 30/365 ≈ 0.0822 years (30-day option)

- Risk-free rate r = 5% annual; no dividends, so b = r = 0.05

- Implied volatility σ = 25%

First compute:

Then:

Numerically:

So

Gamma is 0.0310 per $1 move in S. A $1 move in the underlying causes Delta to shift by about 0.031.

2.3 Practical Notes

-

Hedging Frequency: With Gamma = 0.031, a $1 move in the stock changes Delta by 3.1%. For a $1 million notional position, daily price swings of $1 require adjusting Delta by $31,000 of the underlying to stay hedged.

-

Monitoring: Traders track Gamma not just at spot but across a grid of strikes and maturities (a “Gamma surface”) to see where risk is concentrated.

-

Real-Time Alerts: Set thresholds for Gamma changes; alerts notify traders when Gamma exceeds risk limits.

3 Saddle Gamma: Fast Approximation

3.1 Motivation

For portfolios with thousands of option positions, computing Black-Scholes Gamma for each can be time-consuming. Saddlepoint approximations offer a faster way to estimate Gamma when extreme moves or non-lognormal features matter.

3.2 Saddle Gamma Formula (Lognormal Case)

In Black-Scholes, the cumulant-generating function is

The saddlepoint solves:

so

Substitute into:

Pre-built libraries (in Python or C++) handle these calculations once parameters are specified.

3.3 When to Use

- Short-Dated Options: As T → 0, Gamma spikes; saddlepoint avoids numerical instabilities.

- Heavy-Tailed Models: For fat-tail returns (e.g., jump-diffusion), saddlepoint captures tail behavior more accurately.

- Speed: Reduces CPU time in risk systems recalculating Greeks for large portfolios.

4 Percentage Gamma (GammaP) for Position Sizing

4.1 Definition and Interpretation

measured as basis points of Delta per 1% move in the underlying. Traders use GammaP to compare risk across options on different underlyings.

4.2 Example and Use

Continuing the previous example with S = 100, Gamma = 0.0310

per 1% move.

If a portfolio has $200,000 in option Delta notional at that strike, a 1% move changes Delta by 0.031% of $200,000 = $62. This helps budget hedging costs.

4.3 Risk Limits

Institutions set limits on aggregated GammaP across all options to cap the total Delta shift for a given market move.

5 Gamma Symmetry: Skew Analysis

5.1 Put-Call Symmetry

Gamma symmetry indicates call Gamma at one strike equals put Gamma at a mirrored strike:

where

Traders use this to spot skew: if put Gammas at low strikes exceed call Gammas at mirrored strikes, the market is skewed.

5.2 Application

- Vol Surface Construction: Enforce Gamma symmetry when interpolating to ensure no-arbitrage.

- Skew Monitoring: Compare implied volatilities at K and F²/K; deviations signal directional bias or demand imbalances.

6 VommaGamma: Sensitivity of Gamma to Volatility

6.1 Formula and Calculation

VommaGamma measures how Gamma changes as implied volatility shifts:

6.2 Numerical Example

Using d1 ≈ 0.092, d2 = 0.0203, = 0.0310:

A 1% absolute increase in volatility reduces Gamma by about 0.00124.

6.3 Practical Notes

- Vol-of-Vol Risk: Positions with large VommaGamma are sensitive to volatility shifts. Hedge by trading Vega options.

- Risk Reports: Include VommaGamma exposure to assess how volatility surface moves affect hedging.

7 Speed: How Gamma Changes with Spot

7.1 Formula and Interpretation

Speed is the third derivative :

A negative Speed means Gamma decreases as spot moves away from at-the-money.

7.2 Numerical Example

Using , , , , :

A $0.10 move in spot changes Gamma by approximately −0.0000626.

7.3 Practical Implications

- Dynamic Hedging: Use Speed to estimate additional shares or futures to trade when spot moves a fraction, without recomputing full Gamma.

- Cost Estimates: Estimate transaction costs for small hedge adjustments.

8 Color: Gamma’s Time Decay

8.1 Formula

Color describes

Negative Color indicates Gamma decays as time passes.

8.2 Numerical Example

With , , , , :

For a 1-day (0.00274 years) decay, Gamma decreases by 0.1873 × 0.00274 ≈ 0.00051.

8.3 Use Cases

- Hedging Horizon: When Color is large, Gamma erosion is rapid; hedge more often near expiry.

- Margin Forecasting: Gamma affects margin; use Color to project margin requirements.

9 Implementing in a Risk System

9.1 Workflow

- Market data feed: Ingest live S, implied vols, rates, dividends.

- Batch Greek computation: Compute Γ, GammaP, VommaGamma, Speed, Color daily or on demand.

- Risk dashboard: Show aggregated exposures: total GammaP by underlying, VommaGamma by volatility bucket, largest Speed values.

- Alerts: Notify when Gamma or VommaGamma exceed thresholds or when Color signals rapid Gamma decay.

- Hedge execution: Use Speed and Color to guide size and timing of Delta hedges.

9.2 Sample Python Pseudocode

# Given S, K, T, r, q, sigma

import math

def compute_greeks(S, K, T, r, q, sigma):

b = r - q

d1 = (math.log(S/K) + (b + 0.5*sigma**2)*T) / (sigma*math.sqrt(T))

d2 = d1 - sigma*math.sqrt(T)

gamma = math.exp(-b*T)/(S*sigma*math.sqrt(2*math.pi*T)) * math.exp(-0.5*d1**2)

vomma_gamma = gamma * (d1*d2 - 1)/sigma

speed = -math.exp(-b*T)/(S*S*sigma*math.sqrt(2*math.pi*T)) * math.exp(-0.5*d1**2) * (2 + d1/(sigma*math.sqrt(T)) - d1**2)

color = gamma*(b - (1 + d1*d2)/(2*T))

gamma_p = 100 * gamma/S

return {"Gamma": gamma, "GammaP": gamma_p,

"VommaGamma": vomma_gamma, "Speed": speed, "Color": color}

10 Summary and Best Practices

-

Compute and monitor Gamma and GammaP daily for all liquid strikes; aggregate by maturity buckets.

-

Use VommaGamma to understand how Gamma profiles shift with volatility moves; hedge Vega accordingly.

-

Use Speed and Color to forecast hedging needs when spot moves or time passes.

-

Incorporate saddlepoint approximations in large-portfolio contexts to save CPU time.

-

Validate Greeks by backtesting small price moves to ensure model accuracy in production.