Why Market Structure Choices Determine Who Wins and Who Gets Picked Off

Apr 22, 2026 - Tribhuven Bisen

B-Booking, Last-Look Delays, and the Trust Problem in Crypto Venues

Exchange Microstructure

B-Booking, Last-Look Delays, and the Trust Problem in Crypto Venues

Why Market Structure Choices Determine Who Wins and Who Gets Picked Off

T E C H N I C A L D E E P D I V E

Based on an episode of the Quant Insider Podcast with Annanay Kapila Former Quant Trader at Flow Traders & Tower Research Capital | Co-Founder, QFEX

Introduction

When a trader clicks "buy" on a crypto exchange, they assume their order enters a fair and open marketplace where it competes on equal footing with every other order. In many cases, that assumption is wrong.

A growing number of crypto exchanges operate practices that quietly redirect order flow, add artificial delays to execution, or allow the exchange itself to trade against its own users. These practices, known broadly as B-booking and last-look delays, are not new. They have existed in traditional foreign exchange markets for decades. But the largely unregulated nature of crypto has allowed them to proliferate with far less transparency and oversight than their traditional finance counterparts.

This article examines the mechanics of these practices, explains why they damage liquidity and erode trust, and contrasts them with transparent Central Limit Order Book (CLOB) models. It draws on insights from Annanay Kapila, a former quantitative trader at Flow Traders and Tower Research Capital who now co-founded QFEX, an exchange specifically designed to avoid these structural problems. These insights were shared on the Quant Insider Podcast, hosted by Tribhuvan.

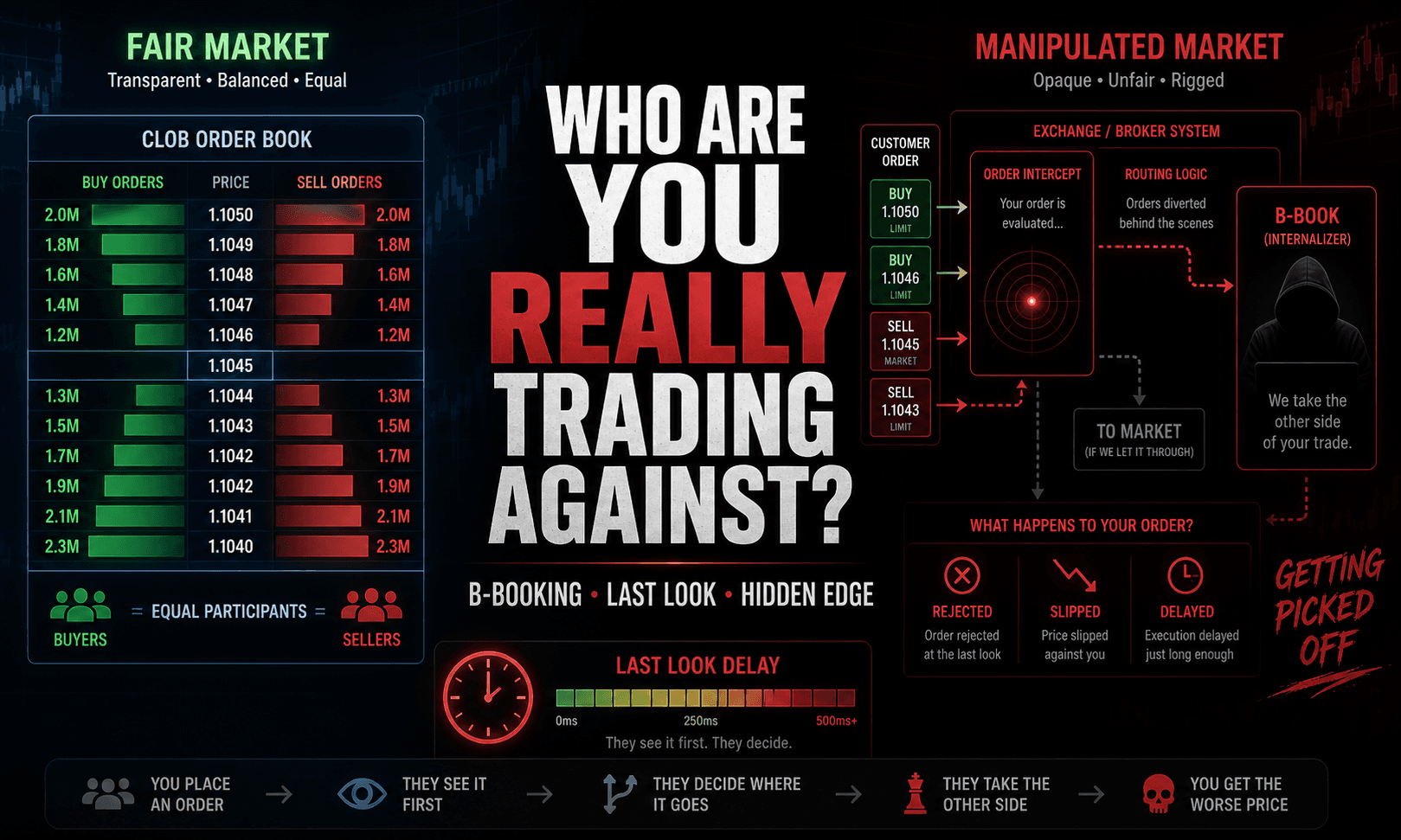

The Central Limit Order Book: The Baseline

To understand what goes wrong, it helps to start with what a fair market looks like. The Central Limit Order Book, or CLOB, is the gold standard for transparent price discovery. It is the model used by major futures exchanges like CME and stock exchanges like NASDAQ.

In a CLOB, every participant sees the same market data. Every order enters the same queue. There is one matching engine processing one instrument in one location. No participant gets preferential access to order flow, and no participant can see or act on orders before they reach the book. The rules are the same for everyone.

The advantages of this model are straightforward. There is no liquidity fragmentation because all trades happen in one place. Price discovery is transparent because all participants contribute to and observe the same order book. Market makers can trust that they are seeing all of the flow, which encourages them to quote tighter spreads and larger sizes. The result is lower transaction costs for everyone.

"That market structure is basically very transparent, very open, everyone is on the same footing, everyone gets the same market data. We're not gonna give anyone any preferential treatment, everyone trades in one place." — Annanay Kapila

The CLOB is not perfect for every use case. Large institutional orders can move the market significantly if executed all at once on a visible order book. This has led to the development of alternative trading systems, dark pools, and other venues that serve specific needs. But for the majority of trading volume, particularly for standardized instruments with many participants, the CLOB remains the most efficient and trusted structure.

B-Booking: When the Exchange Trades Against You

How It Works

B-booking is the practice where an exchange's internal market maker gets first right of refusal on incoming order flow. When a user submits an order, the exchange's internal system evaluates whether that order is likely to be profitable to trade against. If the internal market maker wants the order, it takes it. If it does not, the order passes through to the regular order book where external market makers can fill it.

The term comes from the foreign exchange brokerage world, where firms traditionally maintained an "A-book" of orders that were passed through to external liquidity providers and a "B-book" of orders that the broker kept internally and traded against themselves. The economics are simple: if the broker can identify orders that are likely to lose money (typically retail flow that trades on emotion or poor timing), it is more profitable to take the other side of those trades than to pass them to an external market maker.

Why It Damages Liquidity

The problem with B-booking is not just that it creates a conflict of interest between the exchange and its users. It fundamentally damages the quality of the market for everyone, including the users whose orders are not B-booked.

Here is the mechanism. External market makers on the exchange know, or quickly figure out, that the exchange is cherry-picking the best flow. The orders that reach the external market makers are disproportionately "toxic": they come from informed traders who are more likely to be right about the direction of the market. The profitable, uninformed flow has already been absorbed by the exchange's internal desk.

Faced with this adverse selection, external market makers respond rationally. They widen their spreads to compensate for the higher proportion of toxic flow. They reduce their quoted sizes because they are less confident in their ability to manage risk. Some withdraw from the venue entirely.

The result is a negative feedback loop. The exchange extracts the best flow for itself, which makes the remaining flow more toxic for external market makers, which causes them to reduce liquidity, which makes the overall market worse for all users.

"The other market makers now don't see all the good taker flow, they don't see the orders they can make money on, so they reduce the amount of size they show on the order book." — Annanay Kapila

The Scale of the Problem

B-booking is far more widespread in crypto than most users realize. Kapila recounts attending a conference in Dubai where he met multiple operators running crypto exchanges. Nearly all of them turned out to be running B-books, and many of their users had no idea.

The practice persists because of a mismatch in incentives. Retail traders, who make up the majority of volume on many crypto exchanges, tend to choose platforms based on user experience, branding, and marketing rather than on execution quality. They are often not sophisticated enough to measure whether they are getting good fills, and the exchanges have no regulatory obligation to disclose their B-booking activity.

Kapila notes that many exchange operators he met in Dubai were running B-books without their users being aware. The lack of disclosure is the core problem. B-booking itself can be a valid business model, but only when users know exactly what they are trading against.

Last-Look Delays: The Hidden Execution Tax

How Last-Look Works

Last-look is a related but distinct practice. When a taker submits an order, the exchange or liquidity provider introduces a deliberate delay before executing it. During this delay window, the liquidity provider can observe whether the market has moved. If the market has moved in the taker's favor (meaning the order would be profitable for the taker), the liquidity provider can reject the order or move their price away. If the market has moved against the taker, the order is filled.

The effect is asymmetric. Takers systematically lose their best trades (the ones that would have been profitable) and get filled on their worst trades (the ones where the market moved against them). This creates a consistent drag on taker performance that is invisible unless you are measuring execution quality at the microsecond level.

Impact on Institutional Flow

Last-look delays are particularly damaging for institutional takers. These are sophisticated firms that trade large sizes and rely on precise execution to capture thin edges. When their profitable orders are systematically rejected through last-look, their overall strategy performance degrades.

Kapila reports that QFEX has had direct conversations with institutional takers who refuse to trade on venues with significant delays. Their experience is consistent: they send a buy order, the market moves up shortly after, and instead of getting filled at their original price, the exchange's liquidity moves away during the delay window. The order goes unfilled, and the opportunity is lost.

"We're in conversation with a few taker institutions who want to trade on our platform. They've said, we don't like trading on some of these other venues because they add too many delays. If we send in a taker order, and it's a good taker order, the exchange liquidity will actually move away because there's such a delay before the order gets executed." — Annanay Kapila

This is why QFEX is designed around having the lowest possible latency matching engine. For institutional participants, the ability to get filled reliably on their orders is not a nice-to-have. It is a prerequisite for using the platform at all.

The Spectrum of Market Structures

Not all market structures are equal, and not all B-booking is inherently dishonest. The critical variable is transparency. Kapila identifies a spectrum that ranges from fully transparent CLOBs to undisclosed B-books, with several models in between.

| Model | Examples | How It Works | Trust Level |

|---|---|---|---|

| Pure CLOB | CME, NASDAQ, QFEX | One order book, same rules for all, no preferential access | Highest. Fully transparent. Market makers see all flow. |

| Disclosed Internal MM | Variational, Ostium, Kalshi Trading | Users trade only against the internal market maker. This is clearly disclosed. | Moderate. Users know what they are getting. Works for new asset classes. |

| Firewalled Internal MM | Kalshi (early stage), new exchanges bootstrapping | Exchange operates an internal trading team with a firewall from exchange operations. | Depends on firewall integrity. Acceptable for bootstrapping liquidity in new products. |

| Undisclosed B-Book | Multiple unnamed crypto venues | Exchange cherry-picks profitable flow for its internal desk. Not disclosed to users. | Lowest. Destroys external market maker confidence. Users unknowingly face adverse conditions. |

Disclosed vs. Undisclosed: Where the Line Falls

When Internal Market Making Is Legitimate

There are valid reasons for an exchange to operate an internal market maker. When a platform launches an entirely new asset class, external market makers may not have the expertise, models, or willingness to provide liquidity from day one. Someone has to make the initial market.

Kapila points to Kalshi as a good example. When Kalshi launched prediction market contracts on events like the Super Bowl or election outcomes, external HFT firms had no infrastructure to price these instruments. Kalshi's internal trading arm, Kalshi Trading, provided the initial liquidity. This was a practical necessity, and because Kalshi is regulated by the CFTC, there is meaningful oversight and disclosure around the arrangement.

Similarly, platforms like Variational and Ostium are transparent about the fact that users trade exclusively against an internal market maker. There is no pretense of a competitive order book. Users know exactly what they are getting, and the model can work well for certain use cases.

"As long as it's disclosed, and people know what they're doing, and people know that this isn't an open market competition making these prices, it's the internal market maker, I think that's fine. And in some cases it's a better model." — Annanay Kapila

When It Becomes Deceptive

The problem arises when exchanges claim to operate a fair, open order book while secretly running a B-book on the side. In this scenario, users believe they are trading on a competitive marketplace, but the exchange is selectively intercepting their flow.

This deception has two victims. First, the users whose orders are B-booked are trading against a counterparty (the exchange) that has an informational advantage over them, and they do not know it. Second, the external market makers who believe they are operating on a level playing field are actually receiving adversely selected flow, which degrades their performance and causes them to reduce their participation.

Kapila is direct about this: if an exchange says there is no B-booking but is actually taking half the flow internally, that is a serious breach of trust. The distinction between a legitimate internal market maker and a deceptive B-book comes down to one thing: does the user know?

The Broader Context: OTC vs. Exchange-Traded Markets

B-booking and last-look delays exist within a broader debate about market structure that has been playing out in traditional finance for decades. The core question is whether instruments should trade on centralized, transparent exchanges or in bilateral, over-the-counter (OTC) arrangements.

How OTC Markets Work

In OTC markets, trades happen directly between two parties. There is no central order book. Each trade involves a bilateral agreement, and the terms, including price, can vary from one relationship to the next. The foreign exchange market is the largest OTC market in the world. Despite being traded electronically, FX has no central clearing counterparty. Each trade carries counterparty risk: if the party on the other side of your trade goes bankrupt, you may not get paid.

OTC markets exist because some participants need them. A corporation that wants to hedge a billion dollars of currency exposure does not want to execute that trade on a public order book where the entire market can see the order and front-run it. They go to a bank, negotiate a price bilaterally, and execute in private. This can result in better execution for the specific trade, because the bank may already hold an offsetting position and can offer a tighter price than the public market.

The Case for Electronification and Exchange Trading

While OTC trading serves specific needs, Kapila argues that the overall direction of markets should be towards more electronic, exchange-traded, and centrally cleared models. The reasons are both practical and structural.

Electronification eliminates the inefficiencies of chat-based trading, where a significant portion of European equities volume still flows through chat rooms rather than electronic order books. Exchange trading concentrates liquidity in one place, which leads to tighter spreads. Central clearing removes counterparty risk by inserting a clearing house between every trade, so participants do not need to worry about the solvency of the person on the other side.

The 2008 financial crisis demonstrated the dangers of uncleared OTC markets. When Lehman Brothers collapsed, all of the bilateral swap agreements it had entered into were suddenly at risk. Counterparties who had hedged their exposure through Lehman faced the possibility of those hedges simply evaporating. A centrally cleared model would have insulated them from this risk.

QFEX is built on this principle. By bringing equity perpetual futures onto a central limit order book with integrated clearing, it eliminates the counterparty risk that exists in the OTC swap market while providing the same economic exposure. Users do not need to establish a bilateral relationship with a bank, hire lawyers to negotiate an ISDA agreement, or worry about what happens if their counterparty goes insolvent.

The Robinhood Problem: Opacity and Price Improvement

The tension between transparency and execution quality is not unique to crypto. It plays out in traditional equity markets as well, most visibly in the relationship between Robinhood and Citadel Securities.

Robinhood routes nearly all of its order flow to Citadel Securities, which acts as a designated market maker. Citadel Securities claims it provides better prices than users would get on the public exchange, because its proprietary alpha allows it to price more aggressively. In exchange, Citadel Securities gets access to Robinhood's predominantly retail flow, which is less informed and therefore less toxic than institutional flow.

The claim may be true. But it is extremely difficult to verify independently. The data required to confirm that Robinhood users are receiving genuine price improvement over the public market is not publicly available. It requires analysis of microstructure-level execution data that is accessible only to the firms involved and regulators.

This opacity is the fundamental problem. Even when the arrangement may benefit users in practice, the inability to verify the claim undermines trust. It is the same dynamic that plays out in crypto B-booking: the exchange claims users are getting a good deal, but users have no way to check.

"It's very hard to verify. You have to look at microstructure-level data, which is not public. So it could be that Robinhood users might be getting better pricing, but it's hard to verify." — Annanay Kapila

Why Institutional Flow Demands Transparency

The shift towards transparent, exchange-traded markets is being driven most aggressively by institutional participants. There are several reasons for this.

Measurability. Institutional trading desks measure execution quality obsessively. They track slippage, fill rates, market impact, and effective spread for every order. These firms can and do detect B-booking and last-look behavior by analyzing their execution data. When they identify a venue that systematically rejects their profitable orders or delays their fills, they stop trading there.

Counterparty risk. Institutions that trade OTC swaps carry counterparty risk against the bank or dealer on the other side. Moving to a centrally cleared exchange model eliminates this risk entirely, which reduces the capital they need to hold in reserve against potential counterparty defaults.

Regulatory pressure. In the post-2008 regulatory environment, there is increasing pressure to move OTC instruments onto exchanges or through central clearing. This regulatory direction aligns with the structural advantages of exchange trading.

Consistency. On a transparent CLOB, the rules are known and consistent. There is no ambiguity about whether the exchange is trading against you, whether your orders are being delayed, or whether you are seeing the full order book. This consistency is essential for building the kind of systematic trading strategies that institutional firms rely on.

This demand for transparency is what creates the market opportunity for exchanges like QFEX. By building a venue that is optimized for institutional-grade execution quality, with no B-booking, no last-look delays, and a high-performance matching engine, the platform positions itself to capture the flow that is leaving venues with opaque execution practices.

What Traders Should Look For

For traders evaluating a venue, there are several practical indicators of market structure quality.

Disclosed execution model. Does the exchange clearly state whether it operates an internal market maker, a B-book, or a pure CLOB? If this information is not readily available, that is a red flag.

Fill rate consistency. Track your fill rates on aggressive orders over time. If your profitable orders are consistently not getting filled while your losing orders execute immediately, you may be subject to last-look or selective execution.

Latency transparency. Does the exchange publish data on matching engine latency? A venue that is serious about fair execution will be transparent about its performance characteristics.

Market maker diversity. A venue with multiple independent, external market makers competing for flow is far more likely to offer tight spreads and deep liquidity than one relying on a single internal desk.

Regulatory status. Regulated exchanges are subject to oversight that constrains the most egregious market structure abuses. While regulation is not a guarantee of fairness, it provides a baseline of accountability that unregulated venues lack.

Conclusion

The market structure of an exchange is not a technical detail. It is the single most important factor determining whether users get fair execution. B-booking and last-look delays are not minor irritants. They are structural features that systematically transfer wealth from users to the exchange operator while degrading the overall quality of the market.

The crypto industry is at an inflection point. As institutional capital flows into digital assets and crypto-native financial products like perpetual futures expand into traditional asset classes, the venues that win will be the ones that institutional participants trust. That trust is built on transparency, fair matching, and verifiable execution quality.

B-booking can be a valid business model when it is fully disclosed and when users understand the trade-offs. But the practice of operating undisclosed B-books while claiming to run a fair market is corrosive. It damages market maker confidence, reduces liquidity, and ultimately harms the users the exchange claims to serve.

The direction of the industry is clear. Markets are moving towards electronification, central clearing, and transparent order books. Exchanges that embrace this direction will attract the institutional flow that drives long-term volume growth. Those that rely on opaque execution practices will find themselves increasingly marginalized as participants migrate to venues where the rules are known, consistent, and fair.

About the Source: This article is based on an episode of the Quant Insider Podcast, hosted by Tribhuvan, featuring Annanay Kapila as guest. Recorded in February 2026. Kapila is the co-founder of QFEX, a Y Combinator-backed exchange building perpetual futures for traditional equity markets. He previously traded at Flow Traders and Tower Research Capital.